THE WORKING CAPITAL TRAP THAT KEEPS GOOD MANUFACTURERS POOR

- Novetra Maps

- Jun 3

- 8 min read

THE WORKING CAPITAL TRAP THAT KEEPS GOOD MANUFACTURERS POOR

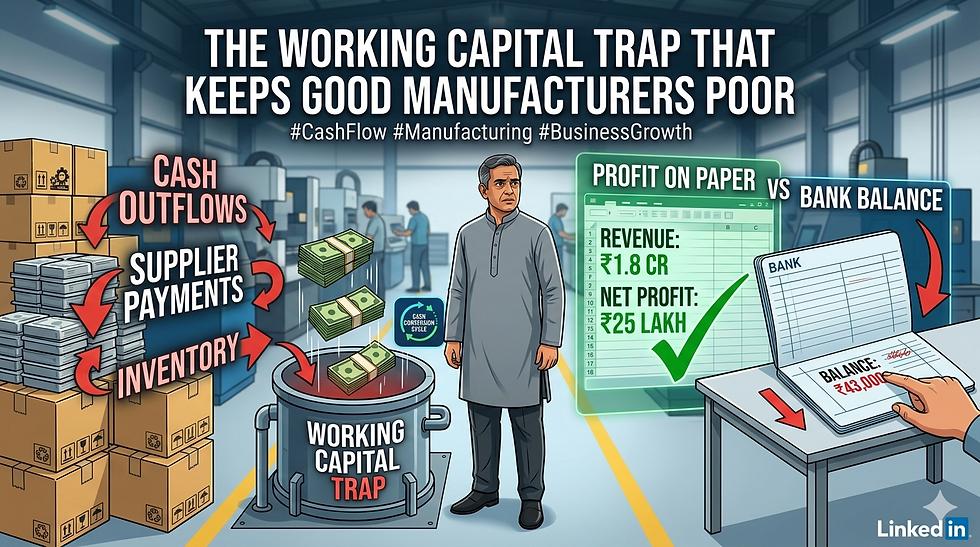

A manufacturer I visited last year showed me his P&L with quiet pride.

Revenue: ₹1.8 crore annually. Net profit margin: 14%. Profit on paper: approximately ₹25 lakh.

Then I asked to see his bank account balance.

₹43,000.

He was a profitable business running on empty.

Every month was a scramble.

Supplier payments delayed.

Staff salary timing managed carefully.

Personal expenses funded by drawing from the business whenever a payment came in.

He wasn't doing anything wrong. His business was genuinely profitable.

But profitable and cash-rich are completely different things. And nobody had ever explained to him why — or what to do about it.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE WORKING CAPITAL TRAP EXPLAINED

Working capital is the money your business needs to fund operations between paying costs and receiving revenue. In manufacturing, this gap is structural and unavoidable.

You pay your supplier to produce goods. That payment leaves your account immediately or within 15-30 days.

Those goods sit in your warehouse. Your money is locked inside finished inventory.

You sell and dispatch. Your money is now locked inside a customer's account receivable.

Your customer pays — in 30 days, 45 days, 60 days, sometimes 90 days.

Only then does the cash return to your account.

The total cycle — from paying your supplier to receiving customer payment — is often 60 to 120 days in Indian manufacturing.

During those 60 to 120 days, your business needs to keep operating. More raw materials. Salaries. Rent. Utilities. Logistics. All of these need payment continuously.

This gap between outflows and inflows is your working capital requirement. And for growing businesses, it expands automatically as revenue grows — because more sales means more inventory, more receivables, more gap to fund.

This is the trap: the better your business does, the more working capital it consumes. Growth can actually make your cash position worse before it makes it better.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHY PROFITABLE BUSINESSES RUN OUT OF CASH

The manufacturer with ₹43,000 in his account despite ₹25 lakh in annual profit was not mismanaging his money.

His working capital cycle looked like this:

Monthly purchases from suppliers: ₹8 lakh, payment due within 30 days.

Monthly sales: ₹15 lakh, customers paying in 60 days on average.

At any given point in time:

Money locked in inventory: ₹12-14 lakh.

Money locked in receivables: ₹28-30 lakh (two months of sales outstanding).

Total working capital deployed: ₹40-44 lakh.

His annual profit was ₹25 lakh. But his working capital requirement was ₹40+ lakh.

He was permanently running a working capital deficit — funded by...

delayed supplier payments,

occasional short-term borrowing, and

the constant stress of timing management.

The profit was real. The cash wasn't there because it was always deployed somewhere in the cycle — sitting in a warehouse or waiting in a customer's account.

Understanding this is the first step. Most manufacturers never have this explained clearly and spend years managing symptoms — delayed payments here, overdraft there — without understanding the underlying structure.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE FIVE LEVERS THAT CONTROL WORKING CAPITAL

Working capital is not fixed. It can be systematically improved through five specific levers.

Lever 1: Reduce Debtor Days

Debtor days — the average number of days it takes your customers to pay you — is the single most impactful lever for most manufacturers.

Reducing debtor days from 60 to 30 on ₹15 lakh monthly sales frees ₹15 lakh in cash. Permanently. Without any other change.

How to reduce debtor days:

Offer early payment discounts. A 1-2% discount for payment within 10 days is often worthwhile for the cash flow improvement it creates. Calculate the annualized cost of the discount versus the cost of the working capital deficit it resolves.

Enforce payment terms contractually. Many manufacturers accept late payment as normal because they've never formalized consequences. A written agreement with late payment interest — even if you never enforce it — changes the psychology of payment priority.

Segment customers by payment behavior. Some customers consistently pay in 30 days. Others consistently pay in 75. Structure your sales effort to favor the reliable payers and limit exposure to the consistently late ones.

Invoice immediately. Every day of delay between dispatch and invoicing is a day added to your collection cycle. Same-day invoicing is a basic discipline that many manufacturers don't practice.

Lever 2: Improve Creditor Days

Creditor days — how long you take to pay suppliers — is the mirror of debtor days.

Extending creditor days from 30 to 45 on ₹8 lakh monthly purchases frees ₹4 lakh in working capital. This is not delaying payment maliciously — it is negotiating payment terms that reflect your relationship and standing as a buyer.

Established buyers with consistent order history have significantly more leverage to negotiate extended terms than they typically exercise.

The conversation with suppliers: "We've been ordering consistently for X years. Our volumes have grown. We'd like to discuss moving to 45-day payment terms from the current 30-day structure."

Many suppliers will agree — especially if the alternative is losing a reliable customer to a competitor who offers better terms.

Important: extended creditor terms should be formally agreed, not informally assumed. Stretching payment without agreement damages supplier relationships and prioritization. Negotiated extension preserves the relationship while improving your cash position.

Lever 3: Reduce Inventory Days

Inventory days — how long goods sit in your warehouse before selling — is the most controllable but most neglected working capital lever.

Every day of inventory sitting unsold is capital that could be deployed elsewhere.

Common inventory problems in manufacturing:

Overstocking slow-moving SKUs. Manufacturers often produce or purchase buffer stock of every SKU equally, regardless of actual demand velocity. The result: fast-moving products run out while slow-moving products pile up.

Producing for forecast rather than demand. Manufacturing to a sales forecast that proves optimistic creates inventory that takes months to clear, locking capital the entire time.

No inventory aging visibility. Without systematic tracking of how long each SKU has been in stock, slow-moving inventory becomes invisible until it's a serious problem.

The minimum fix: track inventory age by SKU. Any item sitting longer than your target inventory days triggers a review — is the price right, is the product being actively sold, is there a channel better suited to moving it?

Lever 4: Improve Cash Conversion on Online Channels

This is the specific working capital advantage of online marketplaces that most manufacturers overlook when evaluating e-commerce.

When you sell through traditional B2B distributors, cash arrives in 30-60-90 days.

When you sell on Amazon or Flipkart, cash settles in 7-14 days.

For the same product, the same sale, the same revenue — the cash conversion cycle is dramatically better on marketplace channels than through traditional distribution.

A manufacturer generating ₹5 lakh monthly through distributors on 60-day terms has ₹10 lakh permanently locked in receivables.

The same ₹5 lakh monthly through Amazon on 7-day settlement has ₹1.2 lakh in transit at any point.

The working capital difference: ₹8.8 lakh freed by channel shift.

This is one of the most underappreciated financial arguments for adding online channels — not just revenue diversification, but meaningful working capital improvement.

Lever 5: Match Financing to Asset Type

Many manufacturers finance working capital with whatever is available — personal savings, overdraft, short-term loans at high rates.

The correct approach matches the type of financing to the type of asset:

Inventory financing: specific facilities exist for financing inventory at rates significantly better than general overdraft.

Receivables financing (invoice discounting): allows you to receive 80-90% of invoice value immediately after raising the invoice, rather than waiting for customer payment. The discount cost is often less than the opportunity cost of the working capital deficit.

Supplier credit: the most overlooked form of financing. Good supplier relationships with favorable payment terms are essentially interest-free working capital financing. Every rupee of extended supplier credit is a rupee of working capital you don't need to borrow.

Understanding which financing mechanism fits which working capital need — and accessing each at its appropriate cost — can reduce total financing costs while improving available cash.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE WORKING CAPITAL CALCULATION EVERY MANUFACTURER SHOULD DO

Before you can improve working capital, you need to measure it.

The basic calculation:

Step 1: Calculate your current working capital cycle

Inventory days = (Average inventory value ÷ Monthly cost of goods sold) × 30

Debtor days = (Average receivables outstanding ÷ Monthly revenue) × 30

Creditor days = (Average payables outstanding ÷ Monthly purchases) × 30

Working capital cycle = Inventory days + Debtor days − Creditor days

Step 2: Calculate your working capital requirement

Monthly revenue ÷ 30 × Working capital cycle = Working capital required

Step 3: Compare to what you actually have available

If your working capital requirement exceeds your available cash plus credit facilities, you have a working capital deficit. This is the silent reason many profitable businesses feel perpetually cash-stressed.

Step 4: Calculate the impact of specific improvements

What happens to your cash position if you reduce debtor days by 15? What if you extend creditor days by 10? What if you reduce inventory days by 8?

Run the numbers for each lever. The improvements that free the most cash with the least business disruption are your priorities.

This calculation takes two hours the first time. It should be done quarterly. Most manufacturers have never done it once.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHAT HAPPENED TO THE MANUFACTURER WITH ₹43,000

We spent one afternoon mapping his working capital cycle.

His debtor days were 67.

Industry average for his category was closer to 42.

His creditor days were 28.

His suppliers were willing to extend to 45.

His inventory days were 54. With better demand tracking, he believed he could get to 38.

The improvement potential across all three levers:

Reducing debtor days from 67 to 45: freed ₹11 lakh in cash.

Extending creditor days from 28 to 42: freed ₹3.7 lakh in cash.

Reducing inventory days from 54 to 40: freed ₹5.6 lakh in cash.

Total working capital improvement: approximately ₹20 lakh.

Not from new revenue.

Not from cutting costs.

From restructuring the timing of money that was already flowing through his business.

Six months later, his bank balance was consistently above ₹15 lakh. The stress of monthly cash management had largely disappeared. He had taken his first proper family holiday in four years.

The business hadn't changed. The cash flow structure had.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THE HONEST TRUTH ABOUT WORKING CAPITAL AND GROWTH

Working capital problems don't get better as businesses grow. They get more complex.

A manufacturer doing ₹50 lakh annually with working capital stress will face the same stress at ₹1 crore — amplified proportionally. The absolute numbers are larger. The pressure is higher. The consequences of getting it wrong are more serious.

The time to understand and fix working capital structure is before growth amplifies the problem — not after it becomes a crisis.

Most manufacturers treat working capital as a finance topic — something for the accountant or CA to worry about. It is actually a strategic topic.

It determines how fast you can grow without external financing.

It determines how resilient your business is to customer payment delays.

It determines whether profitable months feel good or feel like survival.

Understanding your working capital cycle is not complicated. Improving it is not complicated.

It just requires someone to look at it honestly — which most manufacturers, focused on production and sales, never make time to do.

Have you ever calculated your working capital cycle? What's your biggest cash flow challenge?

Drop it in comments — this is one area where practical experience from the community is genuinely valuable.

Comments